😭

Wills • Components of a Will

WILLS#033

Legal Definition

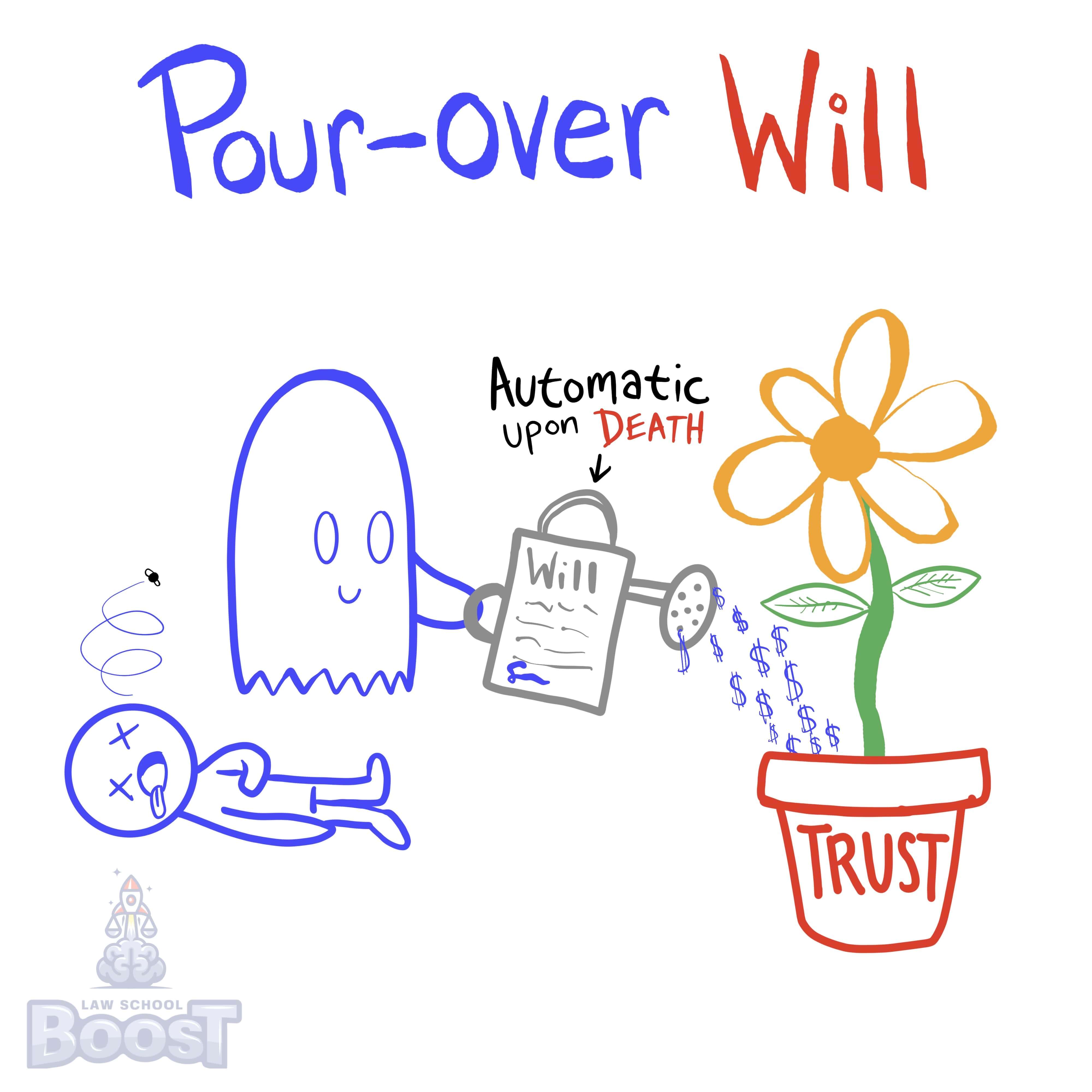

A pour-over will is a legal document that ensures an individual's remaining assets will automatically transfer to a previously established trust upon their death. It is validated through incorporation by reference, acts of independent significance, or can pour over into a valid trust that already exists via the Uniform Testamentary Additions to Trusts Act ("UTATTA").

Plain English Explanation

As you'll learn in the Trust set of cards, trusts are an efficient way to manage access and ownership of assets by packing them into a "trust" and then deciding who gets to use them. In other words, think of a trust as a little red wagon that you pull behind you. You can put all sorts of stuff into your wagon. Real estate, cars, baseball cards, just about anything you want. When you die, rather than the court having to figure out who gets each individual item, you can designate who gets to pick up the handle to the wagon and pull it next. It's a super efficient way to handle transitioning assets between parties.

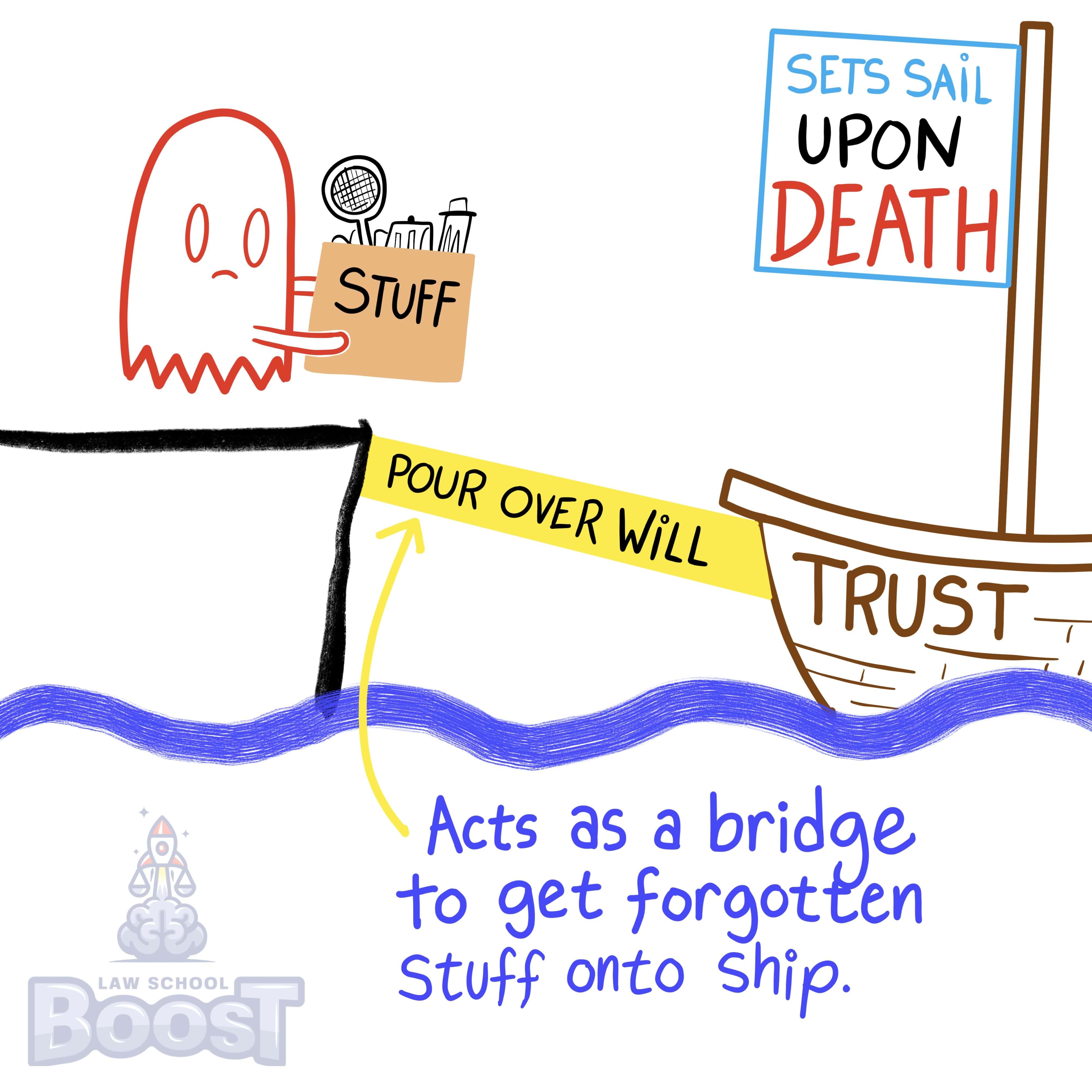

In general, trusts require their creators to identify which property go into them. So if something isn't placed into the trust, then it is not considered to be inside of it. With this in mind, a pour-over will is a legal document where, upon the testator's death, their property is automatically transferred (poured over) into a trust that was already created. It's sort of a fail-safe.

/In other words, a pour-over will ensures property that is not "titled into a decedent's trust" (at the time of their death) is put into the trust via probate. It's a catch-all document used in conjunction with a trust established during the decedent's lifetime.

In general, trusts require their creators to identify which property go into them. So if something isn't placed into the trust, then it is not considered to be inside of it. With this in mind, a pour-over will is a legal document where, upon the testator's death, their property is automatically transferred (poured over) into a trust that was already created. It's sort of a fail-safe.

/In other words, a pour-over will ensures property that is not "titled into a decedent's trust" (at the time of their death) is put into the trust via probate. It's a catch-all document used in conjunction with a trust established during the decedent's lifetime.

Hypothetical

Hypo 1: Bob has a collection of vintage cars and a separate will. He creates a trust for his son, Sam, but forgets to include the car collection in it. In his will, he mentions that any assets not in the trust should go there upon his death. Result: When Bob passes away, the car collection is transferred to Sam's trust through the pour-over will. The will acts like a funnel, ensuring Bob's wishes are respected, and Sam receives the cars.

Hypo 5: Bob creates a trust for his niece but doesn't set up a pour-over will. Later, he inherits a house and doesn't update the trust to include it. Result: Since there's no pour-over will, the house isn't automatically added to the trust after Bob's death. The house goes through a standard probate process instead, showing the pour-over will's necessity in such scenarios.

Hypo 5: Bob creates a trust for his niece but doesn't set up a pour-over will. Later, he inherits a house and doesn't update the trust to include it. Result: Since there's no pour-over will, the house isn't automatically added to the trust after Bob's death. The house goes through a standard probate process instead, showing the pour-over will's necessity in such scenarios.

Visual Aids

Related Concepts

In California, what is the exception to the requirement that an incorporation by reference need be a writing in existence as of the date of executing the will?

What does incorporation by reference require?

What is a codicil?

What is an integration?

What is the doctrine of Acts of Independent Significance?